Media Summary: In this video, we will demonstrate the few steps required to convert the market index S P 500 data into a robust In this video, we will demonstrate the few steps required to convert the market index S&P 500 data into a robust Generalised autoregressive conditional hereroskedasticity (

Garch Volatility Forecast In Excel - Detailed Analysis & Overview

In this video, we will demonstrate the few steps required to convert the market index S P 500 data into a robust In this video, we will demonstrate the few steps required to convert the market index S&P 500 data into a robust Generalised autoregressive conditional hereroskedasticity ( In this video, we'll give an example of how to create an EGARCH model and derive a Master Quantitative Skills with Quant Guild* * Interactive Brokers for Algorithmic Trading* ... Next example is about conditional and conditional

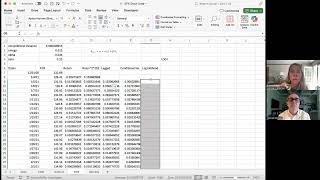

This video demonstrates 3 functions that are part of XlQuant. XlQuant can be obtained free of charge at . In this video Dr. Adamiec sets the stage for the needed data to create a The model that was estimated using C++ code in Xode and is re-estimated here in Corsi (2009) proposed a very simple and intuitive model for the dynamics of variance that utilises realised variance and can be ... Autoregressive conditional hereroskedasticity (ARCH) is very common in financial and macroeconomic time series. How one can ... The market looks calm… then BANG. Chaos everywhere. Most models never see it coming. But one family of algorithms was built ...

Hi all today I like uh to provide you with a simple introduction to These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. Struggling with financial data? Learn the basics in just 30 minutes—for FREE! Sign up now!

![GARCH Volatility Forecast in Excel [UPDATE]](https://i.ytimg.com/vi/FH3c_cxWN0w/mqdefault.jpg)