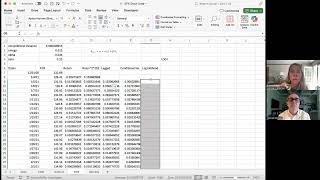

Media Summary: In this video Dr. Adamiec sets the stage for the needed data to create a In this video, we will demonstrate the few steps required to convert the market index S P 500 data into a robust volatility forecast ... Generalised autoregressive conditional hereroskedasticity (

Calculating Garch In Excel Part 1 - Detailed Analysis & Overview

In this video Dr. Adamiec sets the stage for the needed data to create a In this video, we will demonstrate the few steps required to convert the market index S P 500 data into a robust volatility forecast ... Generalised autoregressive conditional hereroskedasticity ( In this video, we will demonstrate the few steps required to convert the market index S&P 500 data into a robust volatility forecast ... The model that was estimated using C++ code in Xode and is re-estimated here in Is the standard deviation of close-on-close stock return the best measure of volatility? Some might argue it is not as it misses ...

In this video, we'll give an example of how to create an EGARCH model and derive a volatility forecast. For more information, visit ... This video demonstrates 3 functions that are The market looks calm… then BANG. Chaos everywhere. Most models never see it coming. But In this video clip I download Volopta C++ code for Duan (1995) and set the components of the project in Visual Studio Community ...

![GARCH Volatility Forecast in Excel [UPDATE]](https://i.ytimg.com/vi/FH3c_cxWN0w/mqdefault.jpg)