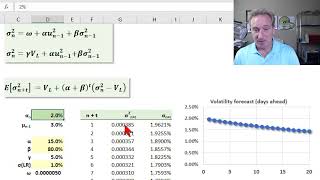

Media Summary: These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. General Autoregressive Conditional Heteroskedasticity model in stock price analysis. Want to learn more? Take the full course at

R Forecasting Volatility Using Garch 1 1 - Detailed Analysis & Overview

These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. General Autoregressive Conditional Heteroskedasticity model in stock price analysis. Want to learn more? Take the full course at Intro to the ARCH (Auto Regressive Conditional Heteroskedasticity) model in time series analysis. The market looks calm… then BANG. Chaos everywhere. Most models never see it coming. But one family of algorithms was built ... This video demonstrates the procedure of fitting a

This video provides some useful guides on how to generate the Full video (72 mins) is a part of 20 hours Financial Analytics