Media Summary: The Jupyter notebook demonstrates how to simulate the Continued presentation of vol surface creation and A brief overview of why I was rejected from Two Sigma.

Option Pricing In Excel Using Heston Stochastic Volatility From Quantlib - Detailed Analysis & Overview

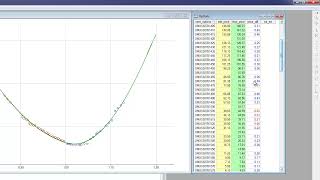

The Jupyter notebook demonstrates how to simulate the Continued presentation of vol surface creation and A brief overview of why I was rejected from Two Sigma. In the last tutorial, I have shown you how to construct all the objects that are required to In 1978, Breeden and Litzenberger showed how under risk-neutral How to create an interest rate yield curve in

Lecture 2022-1: Session 31: Numerical Methods