Media Summary: Master Quantitative Skills with Quant Guild* * Interactive Brokers for Algorithmic Trading* ... Full workshop available at www.quantshub.com Presenter: Roger Lord: Head of Quantitative Analytics, Cardano Within this ... The Wolfram Demonstrations Project contains thousands ...

Heston Stochastic Volatility Model And Fast Fourier Transforms - Detailed Analysis & Overview

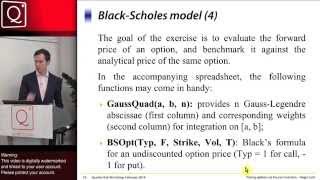

Master Quantitative Skills with Quant Guild* * Interactive Brokers for Algorithmic Trading* ... Full workshop available at www.quantshub.com Presenter: Roger Lord: Head of Quantitative Analytics, Cardano Within this ... The Wolfram Demonstrations Project contains thousands ... Presenter Roger Lord discusses the Black-Scholes Project for the course Functional Programming, prof. Erik Meijer: Library for Quantitative Finance written in Functional and ... Derives the Partial Differential Equation (PDE) that the price of a derivative/option satisfies under the