Media Summary: Why model only one time series at a time? We can do multivariate time series modeling with the vector autoregressive ( Let's take a look at the basics of the vector auto regression model in time series This tutorial shows you how to estimate a vector autoregressive (

Var Estimation And Uses - Detailed Analysis & Overview

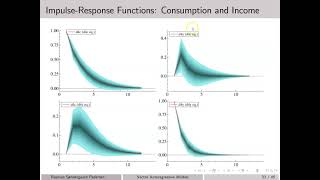

Why model only one time series at a time? We can do multivariate time series modeling with the vector autoregressive ( Let's take a look at the basics of the vector auto regression model in time series This tutorial shows you how to estimate a vector autoregressive ( This is the video associated with QR code QR10.4 in Chapter 10 of Time Series for Data Science: We propose a Bayesian distributed vector autoregressive (DVAR) model to the distributed system with the least square ... I also have the following two related clips:

Dive into the world of financial risk management with this comprehensive guide to Value at Risk ( Video for Econometrics II course at University of Copenhagen (Dept. of Economics). Original slides by Heino Bohn Nielsen and ... This is Lecture 5 in my Econometrics course at Swansea University. Watch Live on The Economic Society Facebook page Every ... Video for Econometrics II course @ Dept. of Economics, Uni. of Copenhagen. Original slides by Heino Bohn Nielsen and adapted ... This video explains the the data structure and This lecture provides an in-depth interpretation of Vector Autoregressive (

The presentation has been prepared with Fabio Parla for the 5th International Statistics Seminar with R. Material ... After watching this video lecture students will understand the basic concept of vector auto regressive model and also know the ...