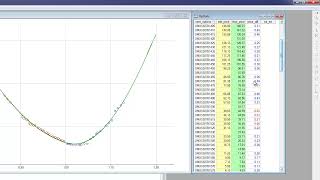

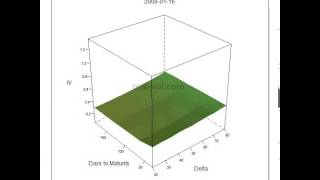

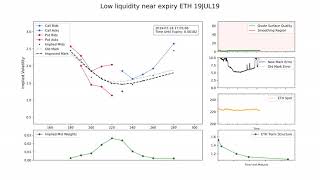

Media Summary: A quick workspace environment tutorial. Where to find and view components such as; - Workspace browser - Code library ... The Heston model is a useful model for simulating stochastic In this video, we introduce the modeling of the implied

Quantlab 101 Calibration Of Vol Surface - Detailed Analysis & Overview

A quick workspace environment tutorial. Where to find and view components such as; - Workspace browser - Code library ... The Heston model is a useful model for simulating stochastic In this video, we introduce the modeling of the implied Reliable option pricing and hedging after the arrival of news that shake the markets requires re- Project: implementation and calibration for SABR model In this video I use MATLAB to generate me an Implied