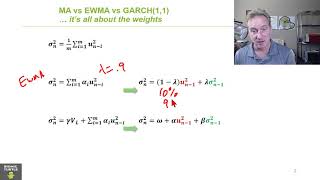

Media Summary: Take the Deep Learning Specialization: Check out all our courses: Subscribe to ... So zero point off start here it didn't look quite would have expected so this would be our The general form for all three is: σ^2(n) = γ*V(L) + α*u^2(n-1) + σ^2(n-1). Discuss this video in our

Frm Exponentially Weighted Moving Average Ewma - Detailed Analysis & Overview

Take the Deep Learning Specialization: Check out all our courses: Subscribe to ... So zero point off start here it didn't look quite would have expected so this would be our The general form for all three is: σ^2(n) = γ*V(L) + α*u^2(n-1) + σ^2(n-1). Discuss this video in our 044 EWMA Exponentially Weighted Moving Average Hacksnation com In this teaser video, I'll dive into a key comparison between the Exponentially Weighted Moving Average is a very important concept to understand Optimization in Deep Learning. It means that ...

Please watch until the end since I mention some important considerations! In this video you will find the steps to calculate the ...