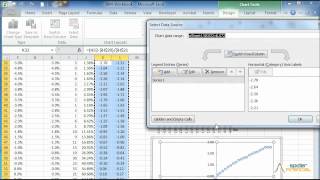

Media Summary: In this video, we demonstrate how to conduct an Autoregressive conditional hereroskedasticity ( In this video, we demonstrate how to run a stationary

Arch Effect Test In Excel With Numxl 1 58 - Detailed Analysis & Overview

In this video, we demonstrate how to conduct an Autoregressive conditional hereroskedasticity ( In this video, we demonstrate how to run a stationary Okay in this values are like already estimated by me and I'll show you how to how to do this in Microsoft In this video, we demonstrate how to conduct a Normality This video simplifies the understanding of the autoregressive conditional heteroscedasticity (

In this video, we'll give an example of how to create an EGARCH model and derive a volatility forecast. For more information, visit ... Discover how to draw area chart under bell curve. To find the area under a normal curve in Beta: simulation functionality is available starting with Kudos to Vaibhav Aggarwal for suggesting this topic! We have already discussed Ljung-Box and Box-Pierce Q- In this video, we give a quick overview of How to model time series heteroskedasticity, particularly for financial data? The most commonly applied

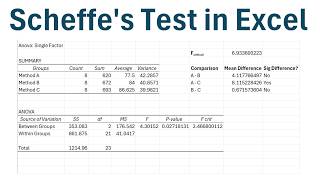

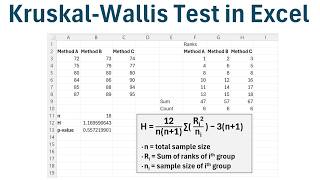

Generalised autoregressive conditional hereroskedasticity (GARCH) is an extension over In this video, I'll guide you through two different methods to create a bell curve in In this video I explain how to perform the Scheffe post hoc A brief tutorial on constructing a GARCH type of model in Microsoft In this video I explain how to perform a Kruskal-Wallis