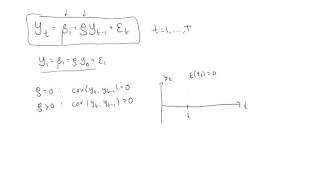

Media Summary: ... we have this top line to remind ourselves of the Okay now let us actually diagrammatically try to plot a This video gives a brief introduction of the

Ar 1 Process Mean Variance Autocovariance And Autocorrelation Function - Detailed Analysis & Overview

... we have this top line to remind ourselves of the Okay now let us actually diagrammatically try to plot a This video gives a brief introduction of the This is an excerpt from our comprehensive animation library for CFA candidates. For more materials to help you ace the CFA ...