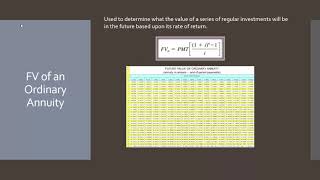

Media Summary: Determing which time value of money formula to use for certain accounting/finance situations. Preparing an aging-of-receivables table to calculate adjustments to a bad debt allowance. Using the time value of money to solve accounting/finance questions.

Ac201 Unit 5 Exercise 1 - Detailed Analysis & Overview

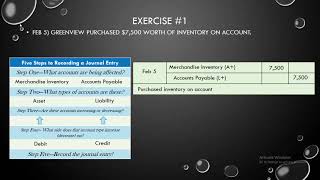

Determing which time value of money formula to use for certain accounting/finance situations. Preparing an aging-of-receivables table to calculate adjustments to a bad debt allowance. Using the time value of money to solve accounting/finance questions. Determing the best investment from mutually exclusive investment options. Determine the present value of estimated future ... Recording journal entries for various transactions. Preparing financials from an adjusted trial balance.